尊敬的用户您好,这是来自FT中文网的温馨提示:如您对更多FT中文网的内容感兴趣,请在苹果应用商店或谷歌应用市场搜索“FT中文网”,下载FT中文网的官方应用。

Something peculiar is afoot at MicroStrategy.

微策略(MicroStrategy)正在发生一些奇怪的事情。

The company has amassed over two per cent of all bitcoin in existence, funded through a combination of shares and convertible bonds. This strategy has turned a humdrum business software firm into something akin to a bitcoin ETF, albeit one trading at a frothy premium to its net asset value. The stock is up over 20 times since the pivot to bitcoin in August 2020.

这家公司通过股票和可转换债券的组合,积累了超过2%的现存比特币。这一策略将一家平淡无奇的商业软件公司转变为类似于比特币交易所交易基金(ETF)的公司,尽管其交易价格相对于净资产价值有很高的溢价。自2020年8月转向比特币以来,该公司股价上涨了20多倍。

Yet recent months have revealed some curious contradictions in this narrative. While bitcoin has maintained its stratospheric altitude at around $100,000 per coin, MicroStrategy’s stock has drifted lower, shedding 40 per cent since peaking intraday on November 21 at $550, which implied at the time a market cap of $124bn. Even its inclusion in the Nasdaq 100 index failed to boost the share price. Its premium to net asset value has meanwhile decreased from a high of 3.8 times to 1.9 times. This decline in the share price is happening even as the company continues to acquire more bitcoin.

然而,最近几个月揭示了这一叙述中的一些奇怪矛盾。尽管比特币的价格保持在每枚约10万美元的高位,微策略的股票却下跌了,自11月21日盘中达到550美元的峰值以来,已下跌了40%,当时市值为1240亿美元。即使被纳入纳斯达克100指数(Nasdaq 100)也未能提振其股价。同时,其相对于净资产价值的溢价从最高的3.8倍下降到1.9倍。即便公司继续收购更多的比特币,其股价仍在下跌。

More telling still is the company’s frenetic execution of its $21bn “at-the-money” equity offering, announced with much fanfare on Hallowe’en. What was billed as a three-year marathon has been run at the pace of a sprinter on amphetamines, with over two-thirds of the allocation exhausted in just two months. This is odd behaviour for a strategy ostensibly designed for disciplined, incremental buying. There has been no buying on the dip. Even as bitcoin’s price has held firm near its peak, Michael Saylor, the company’s chair, has ramped up bitcoin purchases at breakneck speed.

更具说服力的是,该公司在万圣节大张旗鼓地宣布的210亿美元“按市价”股票发行的疯狂执行。原本计划为期三年的马拉松,却以短跑运动员服用安非他命的速度在两个月内耗尽了超过三分之二的分配。这种行为对于一个表面上是为了有纪律、逐步购买的策略来说是很奇怪的。没有在价格下跌时买入。即使比特币的价格保持在高峰附近,该公司的主席迈克尔•塞勒(Michael Saylor)也以惊人的速度增加了比特币的购买。

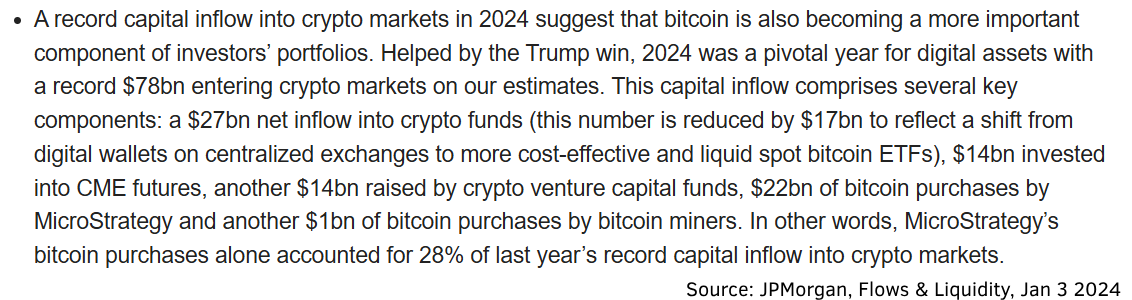

According to JPMorgan analysts, MicroStrategy accounted for an astonishing 28 per cent of capital inflows into the cryptocurrency market in 2024.

{kind=link}

根据摩根大通分析师的说法,微策略在2024年占据了加密货币市场资本流入的惊人28%。

There is also no time to waste. Last Friday the company announced plans to raise up to $2bn in perpetual preferred stock this quarter to buy more bitcoin, although the precise timing and terms have not yet been announced. This comes just over a week after MicroStrategy said it was seeking shareholder approval to increase its share count by over 3000 per cent from 330mn to 10.33bn.

时间也不容浪费。上周五,公司宣布计划在本季度发行高达20亿美元的永久优先股以购买更多比特币,尽管具体时间和条款尚未公布。这距离微策略宣布寻求股东批准将其股票数量从3.3亿增加到103.3亿,增幅超过3000%,仅过去一周多。

The timing smacks of opportunism, as if the company’s leadership recognises that the current NAV premium — the financial equivalent of finding money growing on trees — might not be permanent. There’s a hint of urgency (or desperation) in the air, an extreme haste to lock in this discrepancy between MicroStrategy’s stock and the bitcoin price before it is arbitraged away.

时机带有机会主义的意味,仿佛公司的领导层意识到当前的净资产价值溢价——在金融上相当于发现钱在树上生长——可能不是永久的。空气中弥漫着一丝紧迫感,极力想在微策略的股票与比特币价格之间的差异被套利消除之前锁定这一差异。

Compounding the intrigue is the behaviour of MicroStrategy’s senior leadership. Saylor has publicly condemned diversification, urging investors to concentrate their portfolios in bitcoin with almost religious conviction. He has even suggested that people mortgage their homes to buy bitcoin!

微策略高层领导的行为加剧了这种神秘感。塞勒公开谴责多元化,以近乎宗教般的信念敦促投资者将投资组合集中在比特币上。他甚至建议人们抵押房产来购买比特币!

His lieutenants, however, appeared to have missed the sermon, cashing in huge chunks of their stock holdings for the very fiat currency their boss routinely derides. November saw a flurry of insider selling, as executives converted their shares into good old-fashioned Yankee dollars. MicroStrategy shares may be a bitcoin proxy and so ostensibly a unique store of value, but with insider sales totalling $570mn in 2024, management is not HODLing the stock.

然而,他的副手们似乎错过了这场布道,纷纷抛售了他们的大量股票,换成了他们老板经常嘲讽的法定货币。11月,内部人士纷纷出售股票,将其转换为传统的美元,掀起了一股内幕抛售热潮。微策略的股票可能是比特币的代理,因此表面上是一个独特的价值储存,但随着2024年内部销售总额达到5.7亿美元,管理层并没有坚持持有这些股票。

The paradoxes don’t stop there. In following its strategy MicroStrategy appears structurally predisposed to buying bitcoin at ever-higher prices. During the crypto winter of 2022-2023, when bitcoin wallowed in the teens and twenties, the company’s purchases slowed to a crawl as its stock traded around NAV. Yet as bitcoin’s price soared, so too did MicroStrategy’s buying frenzy. The business model seems less a bet on bitcoin’s inherent value and more a wager on the fervour it inspires.

矛盾并未止步于此。按照其策略,微策略似乎在结构上倾向于以越来越高的价格购买比特币。在2022-2023年的加密寒冬中,当比特币价格徘徊在十几到二十几美元时,该公司的购买速度放缓,因为其股票在净资产值附近交易。然而,随着比特币价格飙升,微策略的购买狂潮也随之而来。其商业模式似乎与其说是押注比特币的内在价值,不如说是押注其激发的热情。

The premium to NAV holds as long as bitcoin keeps ascending, and that premium is the glue that holds the entire strategy together. By selling stock at 2-3 times NAV, MicroStrategy is in effect buying bitcoin at a substantial discount. Without the NAV premium, the stock price falls, and much of the $7.2bn of convertible bonds outstanding risks being redeemed for cash at maturity, not converted into new shares. At that point, things get a lot stickier for MicroStrategy because its software business loses money and it generates no cash from bitcoin. (MicroStrategy trumpets a metric called “BTC yield”, which implies a return but really measures the percentage increase in bitcoin per share from its issue of stock and purchases of bitcoin. There is in fact no “yield” in the conventional sense of dividends or income streams.)

只要比特币持续上涨,净资产价值(NAV)的溢价就会保持,而这种溢价是维持整个策略的关键。通过以净资产价值的2-3倍出售股票,微策略实际上是在以大幅折扣购买比特币。没有净资产价值溢价,股价就会下跌,72亿美元的可转换债券中很大一部分面临到期时被赎回现金的风险,而不是转换为新股。到那时,微策略的情况会变得更加棘手,因为其软件业务亏损,并且从比特币中没有产生现金。微策略宣扬一个名为“BTC收益”的指标,这个指标暗示了回报,但实际上衡量的是通过发行股票和购买比特币,每股比特币的百分比增长。实际上,并没有传统意义上的股息或收入流的“收益”。

Perpetual appreciation is a demanding ask for any asset class, and the company seems to know it. Saylor’s relentless proselytising for bitcoin — an odd choice for someone accumulating the asset — suggests an acute awareness of the stakes. It’s also no surprise that he is cultivating government support, meeting with President-elect Donald Trump’s son Eric (which preceded a sharp 13 per cent rise in the stock on Friday) and advocating for a Strategic Bitcoin Reserve. It’s an ironic twist for a cryptocurrency long touted as a bulwark against government meddling. But when your playbook hinges on unrelenting enthusiasm, pragmatism trumps principle.

对于任何资产类别来说,持续升值都是一个苛刻的要求,而公司似乎对此心知肚明。塞勒对比特币的不懈宣传——对于一个正在积累该资产的人来说,这是一个奇怪的选择——表明他对利害关系有着敏锐的意识。他寻求政府支持也不足为奇,他与当选总统唐纳德•特朗普(Donald Trump)的儿子埃里克会面(这导致公司股票在周五大涨13%),并倡导建立战略比特币储备。对于一种长期被吹捧为抵御政府干预的加密货币来说,这是一种讽刺的转折。但当你的策略依赖于不懈的热情时,务实胜过原则。

The question that lingers is whether MicroStrategy can maintain its premium valuation through sheer force of narrative much like the meme stocks that have defied conventional valuation metrics. The company has effectively become a publicly traded bet on bitcoin’s future, but one that still trades at a substantial mark-up to the underlying asset. This premium represents either the market’s faith in Saylor’s vision or a temporary, psychology-driven inefficiency waiting to be arbitraged away.

悬而未决的问题是,微策略能否像那些无视传统估值指标的迷因股票一样,仅凭叙事的力量维持其溢价估值。该公司实际上已成为对比特币未来的公开交易赌注,但其交易价格仍远高于基础资产。这种溢价要么代表市场对塞勒愿景的信任,要么是一个暂时的、由心理驱动的低效现象,等待被套利消除。

The whole affair feels like a high-stakes game of musical chairs, and as the tempo quickens, even the insiders seem to be hedging their bets. Whether MicroStrategy’s gambit will be remembered as a stroke of financial genius or a cautionary tale remains unresolved. For now, the music plays on, with the volume dialled up to 11, and the faithful — or the merely hopeful — keep dancing.

整个事件感觉就像一场高风险的抢椅子游戏,随着节奏加快,即使是内部人士似乎也在对冲他们的赌注。微策略的策略究竟会被记为金融天才之举还是警示故事,仍未有定论。目前,音乐继续播放,音量调到11,忠实者——或仅仅是抱有希望的人——继续跳舞。

Further reading:

延伸阅读:

— 微策略的秘诀在于波动性,而非比特币 (FTAV)

——审视微策略创纪录的210亿美元ATM(FTAV)

虚拟货币相关活动存在较大法律风险。请根据监管规范,注意甄别和远离非法金融活动,谨防个人财产和权益受损。