2.长寿时代使得带病生存时间延长

2. The age of longevity prolongs the survival in disease

在长寿时代更多疾病将与高龄老人共存,带病生存成为长寿时代的普遍现象。如果将60岁以上老年人寿命分为健康状态和带病状态,就会发现人群预期寿命增加主要是带病生存时间的延长,特别是各种非遗传性慢性病导致的健康损失并不会短期内致人死亡,而是与人长期共存。华盛顿大学健康指标与评估研究所对195个国家和地区的研究表明:1990~2017年间全球绝大部分国家的健康预期寿命③的增速要逊于预期寿命的增速,预期寿命增加7.4年,而健康预期寿命只增加了6.3年(Kyu et al.,2018)。英国学者基于欧洲25个国家的数据研究表明,2005~2011年,65岁老人的预期寿命增加了1.3年,而同期的健康预期寿命没有变化(Brown,2015)。在中国,1993年的中国老年人供养体系调查显示60岁以上老年人在60岁以后的预期寿命中约3/4的时间处于各种慢性病的状态下(王梅,1993)。2018年的第四次中国城乡老年人生活状况抽样调查成果显示中国2018年人均预期寿命是77岁,健康预期寿命仅为68.7岁,存在较大落差。

In the age of longevity, more diseases will coexist with the elderly, and survival in disease will become a common phenomenon. Dividing the lifespan of elderly persons aged 60 years and above into healthy and diseased states shows that the increase in life expectancy mainly comprises an extension of the survival in disease, particularly the loss of health caused by various non-hereditary chronic diseases. These do not cause death in the short term, and coexist with the individual involved over the longer term. The study of 195 countries and regions by the University of Washington’s Institute for Health Metrics and Evaluation shows that between 1990 and 2017, healthy life expectancy (3) in most countries worldwide grew at a slower rate than life expectancy. Life expectancy increased by 7.4 years, while health life expectancy only increased by 6.3 years (Kyu et al., 2018). Using data from 25 European countries, a British study shows that between 2005 and 2011, the life expectancy of a 65 year-old increased by 1.3 years, whereas there was no change in healthy life expectancy over the same period (Brown, 2015). In China, a 1993 survey of the Chinese elderly support system shows that elderly people above the age of 60 spent three quarters of their life expectancy beyond the age of 60 living with some form of chronic disease (Wang Mei, 1993).The results of the 2018 Fourth Sample Survey of the Living Conditions of China's Urban and Rural Elderly shows that China’s average life expectancy in 2018 was 77 years, whereas health life expectancy was only 68.7 years, indicating a relatively large gap.

我们可以看到全球发展趋势表明:越是长寿,带病生存越将成为普遍现象。虽然我们寿命在不断增加,但生存质量则不一定随之变得更好。因此,获得的额外寿命是处于身体健康还是疾病状态这个问题变得越来越重要,如何面对长寿时代带病生存的疾病负担在未来将对卫生系统的规划、健康相关支出和健康产业的发展产生重大影响。

We can see from global development trends that the longer we live, the more likely we are to survive in a disease. Although our life spans are continuously increasing, our quality of life is not necessarily increasing in equal measure. Therefore, the question of whether the extra life is spent in a state of good physical health or in a disease is becoming increasingly important. Finding ways to face the burdens of surviving in disease in the age of longevity will in future have a significant impact on the planning of health system, the expenditures of health-related activities and the development of the health industry.

3.长寿时代将促使健康产业发展

3. The age of longevity will encourage the development of health industry

长寿时代的带病生存使得人们与健康相关的费用支出剧增。据国内外的有关资料,人均医疗费用和年龄密切相关,一般情况下,60岁以上年龄组的医疗费用是60岁以下年龄组医疗费用的3~5倍(李剑阁,2002)。同时,老龄人口规模的增加必然带来社会医疗总费用的增加。日本研究显示,医疗技术进步、经济财富增加、人口老龄化和民众患病结构的不断变化共同导致医疗卫生支出不断攀升,技术进步因素占比40%,为首要因素,其他因素分别占26%、18%和16%(胡苏云,2013)。

Survival in disease in the age of longevity has led to a sharp increase in health-related expenditure. Domestically and abroad, the relevant data shows that the amount of medical expenses per capita is closely related to age. Generally speaking, medical expenses in age groups above 60 years of age are 3-5 times those of age groups below that limit (Li Jian'ge, 2002). At the same time, the increasing size of the elderly population will inevitably lead to an increase in the total cost of social care. Japanese research shows that advances in medical technology, increasing economic wealth, an ageing population and ongoing change in the population’s disease structure have all led to constantly rising medical and health care expenditures. Technological progress accounts for 40% of this, making it the primary factor, while the other factors account for 26%, 18% and 16% respectively (Hu Suyun, 2013).

医疗技术创新是近年推动医疗费用增长的最重要原因之一。回溯医疗技术的发展路径,可以看到研究投入和医疗资源更多地向急性或者致死性疾病倾斜,在消除或延缓与年龄相关的慢性病和细胞变性类疾病方面却投入不够。这种不平衡的投入很大程度上是由于早期研究所处时代的人口结构不同造成的,那时人均期望寿命不超过80岁是常态,带病生存的人口比例较小,对社会的影响也有限。在当前阶段,人口结构已经开始发生重大变化,因此需要重新审视社会资源的分配方式。英国的一项研究显示了这种资源的错配情况,以呼吸道和神经精神类疾病为例,指出两种疾病的伤残调整生命年(DALY)占比分别为8.3%和26.7%,而研究经费占比仅为1.7%和15.3%,表明这两种疾病造成了较大的社会负担却未获得对等的资源投入;此外,癌症的伤残调整生命年(DALY)占比为15.9%,明显低于神经精神类疾病,但研究经费占比却高达19.6%④。目前主流的医疗技术还是以医院内使用的针对重大疾病的治疗手段为主,此类技术的成本和使用门槛高,导致费用昂贵。将患者从医院引流进入基础医疗机构,使用更多低成本的医疗技术,加强疾病预防和健康管理,将不仅对患者自身的健康有利,也将对遏制医疗费用的快速上涨起到积极的作用。

Medical technology innovation is one of the most significant drivers of the growth in medical expenses in recent years. Looking back over the development of medical technologies, we can see that research investment and medical resources have tended to focus on acute or fatal diseases, while there has been insufficient investment in the elimination or delay of age-related chronic disease and cell degenerative diseases. This uneven investment is largely due to the different population structure in the early years of research. At the time, average life expectancy did not normally exceed 80 years, only a small proportion of the population lived with an illness, and the social impact was also limited. At the current stage, however, the population structure has already begun to undergo significant change, and the way in which social resources are allocated therefore must therefore be re-examined. A British study illustrates this mismatch of resources, using respiratory and neuropsychiatric diseases as an example. The study finds that whereas the shares of these two diseases in disability-adjusted life year (DALY) were 8.3% and 26.7% respectively, the shares of research funding for them were 1.7% and 15.3% respectively. It indicates that although these two diseases pose a significant social burden, they have not been allocated equivalent investment resources. In addition, the disability-adjusted life year (DALY) share for cancer accounts for 15.9%, which is significantly lower than that for neuropsychiatric diseases, but the proportion of research funding is significantly higher, at 19.6% (4). At present, mainstream medical technology is still based on the treatment of major illnesses in a hospital setting, where the cost and use threshold for technologies of this kind are high, resulting in high expenditures. Transferring patients from hospitals to entry-level medical institutions, using more low-cost medical technologies, and enhancing disease prevention and health management initiatives will not only benefit the patient’s own health, but will also play a positive role in curbing the rapid increase in medical costs.

我们可以预见到,长寿时代将促使健康产业结构升级。在长寿时代,随着人体的衰老,不可避免地出现相关健康问题,带病生存成为常态,健康将成为个体关注的第一要素和最宝贵财富。第四次中国城乡老年人生活状况抽样调查显示老年人照护服务需求持续上升:2015年,我国城乡老年人自报需要照护服务的比例为15.3%,比2000年的6.6%上升近9个百分点;城乡老年人的居家养老服务需求项目排在前三位的分别是上门看病、上门做家务和康复护理,其比例分别是38.1%、12.1%、11.3%。这些都是老年人群庞大的潜在需求,目前来看,只有部分社区提供这些服务,大部分社区都存在供给短缺(杨晓奇、王莉莉,2019)。

We can foresee that the age of longevity will encourage the upgrading of the structure of the health industry. In the age of longevity, health problems associated with physical ageing will inevitably appear, survival with illness will become increasingly normal, and health will become an individual’s primary focus of concern, as well as one of their most precious assets. The Fourth Sample Survey of the Living Conditions of China's Urban and Rural Elderly shows that demand for elderly care services continues to increase: in 2015, the proportion of elderly individuals in urban and rural areas of China who self-declared a need for care services stood at 15.3%, an increase of nine percentage points over the 6.6% figure for 2000; the three most common home and elderly care services requested by the elderly in urban and rural areas were home visits for medical care, home housework-support visits, and rehabilitation care, making up 38.1%, 12.1% and 11.3% of the total respectively. There is huge potential demand from the elderly population, and at present, only a limited number of communities provide such services. The vast majority of communities suffer from supply shortages in this area (Yang Xiaoqi and Wang Lili, 2019).

长寿时代,庞大的健康需求将促进大健康产业的极大发展。为人们提供健康生活解决方案,是大健康产业最大的商机,也将推动社会进入健康时代。在美国,卫生总支出占GDP的17.9%,大健康是最大的产业。美国65岁及以上老人占总人口比例为16%,卫生总支出占比达到36%;如果从55岁算起,29%的人口花费了56%的卫生支出⑤。目前,中国的经济结构中,房地产占比最高,其次是汽车,卫生总费用在GDP中占比仅有6.4%。

In the age of longevity, massive demand for health will encourage the outsized development of the health industry. Providing people with healthy living solutions will be the health industry’s most significant commercial opportunity, and will also drive society into a new era of health. In the United States, total health expenditure makes up 17.9% of GDP, and health is the country’s largest industry. The elderly, 65 years and above, make up 16% of the US’s total population, and health expenditure in this segment accounts for 36% of the total. If calculated from the age of 55 onwards, 29% of the population spends 56% of total health expenditure (5). Currently, real estate accounts for the largest share of China's economic structure, followed by automobiles, while total health expenditure only accounts for 6.4% of GDP.

健康时代里最核心的产业是医药工业、健康服务和健康保险。2019年《财富》世界500强榜单中,美国有15家大健康企业,中国只有2家算是大健康企业。按照《“健康中国2030”规划纲要》的目标,到2020年,中国健康服务业总规模超8万亿元,2030年达16万亿元。可见,中国大健康产业具有巨大成长空间和产业结构转变机会,未来有望成为中国经济中的支柱产业之一。

The core sectors in this era of health are the pharmaceuticals, healthcare services and health insurance industries. The 2019 Fortune Global 500 included 15 health conglomerates in the USA, whereas in China, only two companies could be considered as health businesses. In line with the objectives set forth in the outline for Healthy China 2030, the total scale of Chinese healthcare services will exceed CNY 8 trillion by 2020, and CNY 16 trillion by 2030. It can be seen that China’s health industry has huge potentials for growth and opportunities for industrial structural transformation, and it is expected to become a pillar industry in China’s future economy.

(三)长寿时代与财富时代

(c) The age of longevity and the era of wealth

长寿时代,人们的预期寿命延长,居民高度关注养老资金是否充沛。在公共养老资金有限的情况下,理性人将更有动机增加财富总量和延长财富积累期限来储备养老资金,形成旺盛的财富管理需求,因此,与长寿时代相伴而生的是财富时代。

Human life expectancy rising extending in the age of longevity, and there is widespread popular concern over whether pension funds will provide sufficient coverage. Against a background of limited public pension funds, sensible people will be motivated to increase their total wealth, and extend the period over which they accumulate wealth in order to save for their pension funds, generating strong demand for wealth management services. This means that the age of longevity will be accompanied by an era of wealth.

1.长寿时代,养老金替代率是关键

1. In the age of longevity, the pension replacement rate is key

根据生命周期理论,人的储蓄行为受所处年龄阶段影响(Ando and Modligliani,1963)。年轻时提供劳动力增加储蓄,老年时用于消费。随着预期寿命的增加和预期抚养比的上升,个体会通过调整消费和储蓄行为、年轻时增加资本积累等方式应对延长的老年生活消费所需(Lee and Mason,2006),以保证充足的替代率(平均养老金与社会平均工资之比)满足平滑消费,实现与生命等长的现金流。

According to life cycle theory, people’s saving behaviour is influenced by their stage of life (Ando and Modigliani, 1963). When they are young, they provide labour to increase their savings, which they subsequently spend in their old age. As life expectancy and the expected dependency ratio rise, individuals will respond by adjusting their consumption and savings behaviour, and increasing their accumulation of capital while they are young, amongst other means, to meet the needs of their extended old age lifestyle (Lee and Mason, 2006), to ensure a sufficient replacement rate (the ratio of the average pension to the average social wage), and thus ensure uninterrupted consumption and cash flows throughout the length of their lives.

在老龄人口占比增多的背景下,公共养老金会持续承压,老年抚养比的上升和领取养老金年限的延长势必会导致狭义养老金替代率的下降。而广义养老储蓄资本(包括公共养老金和个人养老储备)在提前筹划尽早储备的前提下可以实现随老龄人口占比增多而提高。2019年墨尔本美世养老金指数报告样本国家数据显示,养老金充足率指数与老龄人口占比呈现正相关性,相关系数为58%。养老金指数排名前三的荷兰、丹麦,其养老金结余资本与GDP之比分别是173.3%和198.6%,且随着老龄人口占比的增加呈上升趋势。荷兰、丹麦等国家老龄人口占比更高,但因为鼓励养老储蓄政策的存在,养老资金储备保持了较高的充足率。

In the context of an increase in the proportion of the elderly population, pressure on public pensions will continue to rise, and the increase in the old-age dependency ratio as well as the extension of the pension period will inevitably lead to a drop in the pension replacement rate in its narrow sense. However, pension savings capital in the wider sense (including public pensions and private pension savings) can still be increased as the elderly proportion of the population grows, provided that planning for reserves is started as soon as possible. Sample country data from the 2019 Melbourne Mercer Global Pension Index shows that the pension adequacy ratio and the proportion of the elderly population have a positive correlation, with a correlation coefficient of 58%. The Netherlands and Denmark, which both rank in the Top 3 of the pension index, have ratios of pension surplus capital to GDP of 173.3% and 198.6% respectively, both of which are trending upwards as the elderly proportion of the population increases. Although the elderly proportion of the population is higher in countries such as the Netherlands and Denmark, pension fund reserves have maintained a relatively high adequacy ratio because of the existence of policies that encourage pension savings.

根据国家统计局数据显示,自1997年中国城镇居民基本养老体系改革以来,养老金社会平均工资替代率从71.51%降至45.92%。在广义养老金总量上,与发达国家相比,中国的养老资金储备有待提高。中国养老金三支柱占GDP的比重仅为8%,OECD国家平均占比为49.7%,而美国的占比也达到146%(孙博,2018)。在养老金结构上,中国的养老储备严重依赖第一支柱,第二支柱和第三支柱占比过低。由于企业负担和经济结构的差异,中国发展第二支柱养老体系迟缓,亟须提高第三支柱占比,让个人养老保险发挥更大作用。

National Bureau of Statistics data shows that since the start of reforms to the basic pension system for urban residents in China in 1997, the social average wage replacement rate for pensions has dropped from 71.51% to 45.92%. In terms of the total pension amount in the wider sense, China's pension fund reserves need to be increased in comparison to developed countries. The three pillars of Chinese pensions only account for 8% of GDP, whereas the average for OECD countries is 49.7%; in the USA, the figure is 146% (Sun Bo, 2018). In terms of the pension structure, China's pension reserves are heavily reliant on the first pillar; the second and third pillars provide too low a proportion of this support. Due to differences in corporate burdens and the economic structure, China has been slow to develop the second pillar of its pension system, and further support from the third pillar is urgently required in order to enable personal pension insurance to play a greater role.

2.长寿时代带来财富的增长

2. The growth in wealth brought about by the age of longevity

在人口红利理论之后,人口经济学家提出第二次人口红利理论,即理性人会调整自己的消费和储蓄行为、人力资本投资行为、劳动力供给行为,以应对长寿时代的各项挑战(Disney,2000;Lee and Mason,2006;蔡昉,2009)。

In line with demographic dividend theory, demographic economists proposed a second demographic dividend theory, namely that sensible people would adjust their own consumption and saving, human capital investment and labour supply behaviours to meet the challenges of the age of longevity (Disney, 2000; Lee and Mason, 2006; Cai Fang, 2009).

人力资本在第二次人口红利形成中起到重要作用。经济学家卢卡斯将人力资本定义为“其质量取决于教育程度的有效劳动力”(Lucas,1988)。人力资本的重要成分包括健康和教育,在上一节我们已经对健康进行了讨论,这里我们将重点放在教育。个人层面,教育水平提高有利于受教育者竞争力的提升,促进职业生涯发展和工资收入提高。预期寿命的提高可以激励教育投入。个体理性预期的调整包括基于人力资本积累预期的教育年限和教育投资调整(杨英、林焕荣,2013)。预期寿命的提高使得教育投入的受益时间拉长,个体更有激励进行教育投资(Hansen and Lønstrup, 2012;Cervellati and Sunde, 2013)。宏观层面,老龄人口占比提升加速产业结构调整,劳动密集型产业让渡给资本、技术密集型产业,人力资本的价值更加重要。世界银行数据显示,预期寿命越长的国家受教育水平越高。预计中国劳动人口平均受教育年限将从2018年的10.5年上升至2035年的12年。总之,人力资本的质量提升将促进劳动生产率提升,居民收入水平亦将随之增加,进而促进社会财富总量的发展。

Human capital plays a major role in the formation of the second demographic dividend. Economist Robert Lucas defined human capital as effective labour whose quality is dependent on the level of education (Lucas, 1988). Major components of human capital include health and education. In the previous section, we discussed health, and here, we will focus on education. At the personal level, improving education standards is conducive to enhancing the competitiveness of the educated individual, promoting their career development and boosting their wage income. Increased life expectancy can stimulate investment in education. Adjusting the rational expectations of an individual can include adjustments to their years spent in education and to their investment in education based on human capital accumulation expectations (Yang Ying, Lin Huanrong, 2013). Increases in life expectancy extend the period of time over which the benefits of investment in education are reaped, making individuals more motivated to invest in education (Hansen and Lønstrup, 2012; Cervellati and Sunde, 2013). At the macro level, the increase in the elderly proportion of the population accelerates adjustments to the industrial structure: labour-intensive industries give way to capital- and technology-intensive industries, and the value of human capital plays an even more important role. World Bank data shows that countries with longer life expectancy have higher levels of education. It is forecast that the average years of education received by China’s working population will increase from 10.5 years in 2018 to 12 years in 2035. In short, improving the quality of human capital will promote improvements in labour productivity, and income levels will increase accordingly, further promoting the overall development of social wealth.

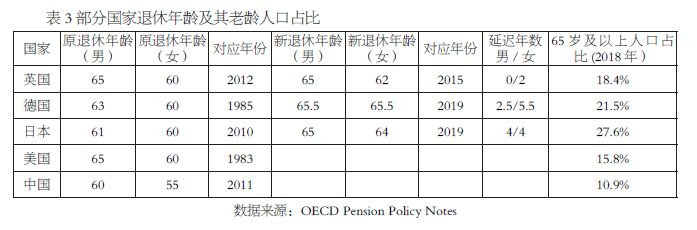

养老财富积累期限的延长,也将促进社会财富总量的发展。伴随着人口预期寿命延长与健康水平提升,健康低龄老人人数将大幅增加,叠加教育投入增加带来的人力资本质量提升,人力资本的折旧将放缓,该人群具备延长工作年限的基本条件。如果劳动人口的工作年限延长,其养老的财富储备期限将延长。事实上,多个老龄人口占比较高的国家采取了延迟法定退休年龄的方式来作为应对措施之一。此外,为应对长寿时代,理性人会在年轻时期更早地开始筹划养老的财富储备。以上两种方式都将延长养老财富储备的期限,提升社会财富总量。(见表3)

Extending the period over which old-age wealth is accumulated will also promote the development of a society’s total wealth. With the increase in the population’s life expectancy and improved health, the number of healthy young elderly (i.e. people aged 55-75) will increase substantially. As the increase in investment in education will boost the quality of human capital and the depreciation of human capital will slow, this population segment now fulfils the basic criteria for extending their working lives. Extending the working lives of the working population means that the period over which they accumulate wealth for their pensions will also be prolonged. In fact, many countries in which relatively high proportions of the population are elderly have chosen to delay the legal retirement age as a countermeasure. In addition, in response to the age of longevity, sensible people will start to plan their pension savings at an even earlier stage in their lives. Both of these methods will extend the duration of wealth accumulation for old age, and increase the total wealth of a society (See Table 3).

3.长寿时代居民的财富管理需求引领财富时代

3. Wealth management needs in the age of longevity will open up an era of wealth

长寿时代,居民将更加依赖投资回报和财富积累来养老,财富管理需求旺盛,长寿时代将带来财富时代。随着老龄人口总量和比例快速增长,公共养老金替代率呈下降趋势。同时,少子化使得依靠子女养老的可能性下降。因此,个人和家庭的投资回报对于居民养老的重要性提高。以中国、美国、日本、英国、德国等老龄人口占比较高的国家近20年的数据为例,随着老龄人口占比的不断提升,个人财富市场规模也持续增加。而且,一国个人财富市场规模与GDP的倍数关系基本趋于稳定,甚或上升。例如,根据瑞信2019年全球财富报告(Global Wealth Report 2019)显示,近20年来,中国的老龄人口占比从7%上升至12%,个人财富市场规模从4万亿美元上升至64万亿美元,占GDP的比例从3.1倍上升至4.7倍,倍数呈持续上升态势;同期,美国的老龄人口占比从16%上升至19%,个人财富市场规模从42万亿美元上升至106万亿美元,占GDP的比例从4.1倍上升至5.2倍,倍数呈上升趋势。

In the age of longevity, people will increasingly rely on returns on investment and the accumulation of wealth to provide for their old age. This will create strong demand for wealth management, and the age of longevity will usher in an era of wealth. As the elderly population grows rapidly, in terms of both total numbers and their proportion of the total population, public pension replacement rates will record a downward trend. At the same time, the reduction in the birth rate reduces the possibility of relying on one’s children in one’s old age. Because of this, personal and family returns on investment have become more important to people’s pensions. If we look at data for the last 20 years in countries with relatively high proportions of the elderly in the population, such as China, the USA, Japan, the UK and Germany, the scale of the personal wealth market has continued to grow as the elderly proportion of the population has increased. Moreover, the relationship between the scale of a country’s personal wealth market and its multiple of GDP has basically stabilised, or even increased. For example, according to Credit Suisse’s Global Wealth Report 2019, over the last 20 years, the elderly proportion of the Chinese population has increased from 7% to 12%, whereas the scale of its personal wealth market has increased from USD 4 trillion to USD 64 trillion. The ratio of the scale of personal wealth market to GDP also increased from 3.1 to 4.7 , and this multiple is continuing to rise. Over the same period, the elderly proportion of the US population increased from 12% to 16% , the scale of the personal wealth market grew from USD 42 trillion to USD 106 trillion. The ratio of the market scale to GDP, which increased from 4.1 to 5.2 , is continuing an upward trend.

财富时代,中国居民财富结构将更加多元化。居民财富管理将直接影响居民消费,包括老年时期消费。根据西南财经大学与广发银行联合发布的《2018中国城市家庭财富健康报告》,中国居民财富管理的结构不合理,主要表现为家庭住房资产占比过高(70%),远高于美国的31%,严重挤压了金融资产配置。下一步,中国居民财富从房地产向金融资产转移预计将是大趋势,中国居民财富结构将更加多元化。另外经历资本市场洗礼,个人投资者开始变得更加理性,更加成熟,更倾向于向专业的财富管理机构寻求投资建议。瑞信2019年全球财富报告中也指出,中国人均财富在近20年间从4293美元提升至5.85万美元,增长了13倍;同期,与美国相比,中国人均财富水平从美国的1/49上升至1/7.5,仍有较大提升空间。随着中国经济的持续发展,中国人均收入水平也将不断提升,个人财富市场规模将持续成长。

In the era of wealth, the household wealth structure of Chinese people will become more diversified. Wealth management will have a direct impact on consumption, including consumption in old age. According to the 2018 Wealth and Health Report for Chinese Urban Families jointly published by Southwestern University of Finance and Economics and China Guangfa Bank, the wealth management structure of Chinese citizens is currently irrational, mainly due to the excessively high proportion of domestic housing assets (70%), far higher than the US figure of 31%, and this forms a severe constraint on the allocation of financial assets. Next, the transfer of Chinese individuals’ wealth from real estate to financial assets is expected to become a major trend, and their household wealth structure will become more diversified. In addition, as they become more experienced in the capital markets, individual investors have begun to take a more rational and mature approach, and are more inclined to seek investment advice from professional wealth management institutions. The Credit Suisse Global Wealth Report 2019 also notes that over the past 20 years, China’s per capita wealth has grown from USD 4293 to USD 58, 500, a 13-fold increase. Over the same period, compared to the US, China’s per capita wealth has increased from 1/49 of the US level to 1/7.5, meaning that there is still plenty of room for improvement. As the Chinese economy has continued to develop, China's per capita income will also continue to increase, and the size of the personal wealth market will continue to grow.

综上所述,长寿时代人口年龄结构将逐步形成新均衡,并以低死亡率、低生育率、预期寿命持续提升、人口年龄结构趋向柱状、平台期老龄人口占比超越1/4为主要特征。在长寿时代下,人类疾病谱转向慢性非传染性疾病,对健康寿命的关注将产生庞大的需求,促使健康产业结构升级,推动社会进入健康时代。同时,在长寿时代养老金替代率成为关键,人力资本质量提升、养老财富积累期限延长将促进社会财富总量的发展,个人消费、储蓄、财富积累的方式会为之改变,财富管理的旺盛需求将引领财富时代。随着人类迈入长寿时代,健康时代和财富时代必然随之到来,需要用大健康的视角系统性地分析三者的关系。

In summary, the age structure of the population in the age of longevity will gradually establish a new equilibrium, characterised by low mortality and fertility, a continuing rise in life expectancy, a population age structure tending to become pillar-shaped, and an elderly proportion of the population which exceeds one quarter of the total during the plateau period. In the age of longevity, the spectrum of human disease will switch to chronic non-communicable diseases. The focus on a healthy lifespan will generate massive demand, promote a structural upgrading of the health industry, and drive society into an era of health. At the same time, the pension replacement rate will become key in the age of longevity. Improvements in the quality of human capital and the extension of the period of time over which old-age wealth is accumulated will promote the development of a society’s total wealth, and the ways in which individuals consume, save and accumulate wealth will change. Strong demand for wealth management will usher in an era of wealth. As mankind steps into the age of longevity, an era of health and an era of wealth will inevitably follow, and the relationship between the three of these must be systematically analysed from a broader perspective of healthcare.